An audit report on financial statements is the accounting engagement that provides the greatest insurance to the financial statements’ reader that they present a true and fair view of the Condominium Corporation’s financial position. Such an engagement is often requested by investors or banker when a company requires substantial external financing.

In Co-ownership, at least in Quebec, it is much less frequently requested, mainly because of costs. Many Condominium Corporations that want to have their financial statements produced by an independent accountant will instead turn to a review engagement. It is interesting to note, that the “Condominium Act” of Ontario requires all Co-ownership of more than 24 units to have their financial statements audited annually prior to their annual meeting, which must be held within 6 months.

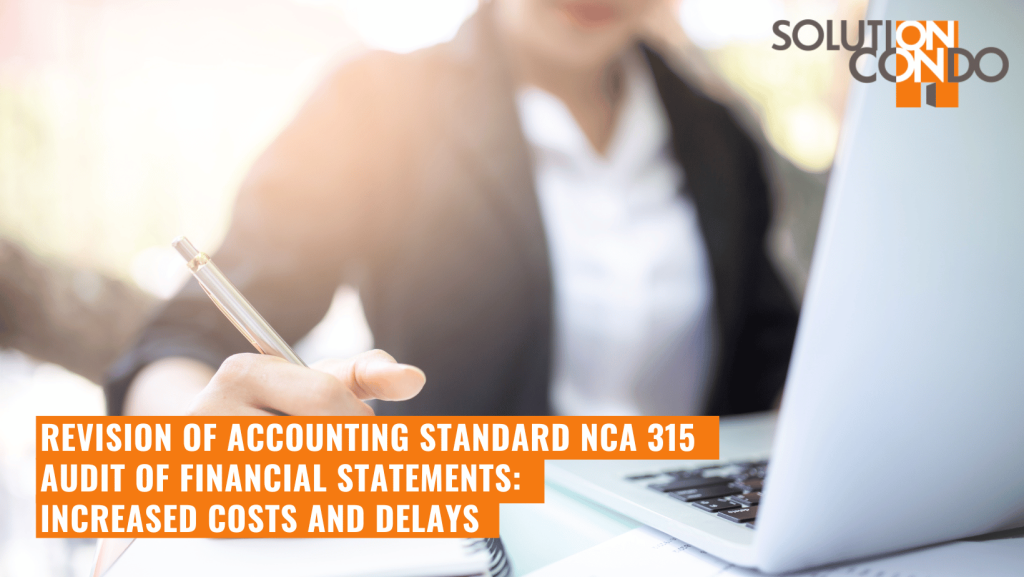

If you have your financial statements audited, you’ll see that the costs and time of production has been increasing for some time. This is mainly due to the additional work that accountants must do as a result of the revision of the CAS 315 accounting engagement.

During an audit engagement, the accountant performs a risk assessment of the audited entity before carrying out sample tests.

In general, a Condominium Corporation is a relatively low-risked entity in terms of the organizations inherent risk since its activities are simple (cash inflow related to condo fees, cash outflow related to expenses, which are generally approved by 1 or 2 members of the Board of Directors) and few in number.

The second risk that an accountant must evaluate is control risk. The accountant must document certain procedures that enable them to understand how financial information is compiled and validated by those responsible for keeping the Condominium corporation’s books. This includes, for example, risks that may arise from inadequate separation of accounting functions (check issue, bank reconciliation, deposit, supplier creation, journal entry, financial statements’ closing) or approval and validation procedures for tasks affecting the quality of financial information.

That being said, in the past, accountants often assessed risk in a general way. They would document inherent risks and control procedures, and they would assess the level of risks and then could make recommendations to the audited organization to improve its processes and thus reduce the level of risk perceived by the accountant. Accountants were not necessarily required to test control in depth to establish that an entity’s level of risk was low.

Obviously, it is this risk level that influences the size of the samples the accountant will have to test, which consists of corroborating a certain number of probable elements (invoices, deposits, contracts, etc.) that will enable them to obtain a sufficient level of comfort to issue their audit report without reservation.

The higher the risk, the larger the samples to be tested, which has a direct impact on the level of work required of the accountant to be able to give an opinion.

With modernization of CAS 315 engagement, accountants must now consider the general controls over information technology (GITC) when assessing the level of control risk, since they can have a significant impact on financial data. Furthermore, for all control risks, including those related to GITC, if the accountant does not make tests to confirm the proper functioning of these controls, they must now consider the audited entity’s level of risk to be “high”.

To have to test general controls around technology information (GITC) will mean that for organizations with relatively few financial transactions (the vast majority of Condominium Corporation), the accountant will have no other choice but to document the control environment as in the past to have a good understanding of it, but will not test the controls in order to be able to reduce the level of risk, as the additional work involved will not be worth it.

In fact, as the subsequent time saved (by reducing the size of the audit probable elements samples) for testing the GITC would not be sufficient compared to the work invested upstream, the accountant will have to assess the audited entity’s risk as “high”, with the consequent need for additional corroboration work than in the past.

As a result, revision of CAS 315 engagement means additional work for accountants, both upstream by testing the control environment, and downstream by increasing the number of probable element samples to be tested.

The revision of this engagement was however to be expected as the technological and regulatory environment continues to become more complex for organizations, which are increasingly using complex software with a high degree of automation. In this context, the identification and evaluation of risks are a very important step, as they form the basis for the design and implementation of audit procedures to identify material misstatements or errors in financial statements.

Given the inevitable increase in workload for audit accountants, firms will have to gradually adjust their staffing levels and pricing. However, we can already sense that, in a context of labor shortages that is hitting the accounting sector hard, this adjustment is not easy for firms, and many of them have longer-than-usual delays for producing financial statements. Please bear with them, as they are working very hard to adjust to the new standards imposed on them.

Elise Beauchesne, CPA, Adm.A

Associate, Solution Condo Inc.

![]()

![]()

![]()

![]()

Arbitration co-ownership condo copropriété déchets Entretien formation Gestion Immobilière loi 31 Médiation Partnership Property Management propertymanager prévention Prévention des sinistres Real Estate brokerage RGCQ Taxes Ville Water damage împôt

Gestion autonome, à la carte

ou complète, nous avons

une formule pour vous.

Notre code de conduite vous

assure une gestion responsable

et transparente.

Avec notre Intranet privé exclusif,

vous avez accès aux informations

de votre syndicat en temps réel.

Optez pour la tranquillité d’esprit

avec notre service d’appels d’urgence

24 h par jour, 7 jours sur 7.

![]() Unique software

Unique software

![]() Save - time and money

Save - time and money

![]() Flexibility

Flexibility

![]() Multidisciplinary team

Multidisciplinary team

Contact information

1751, rue Richardson

Bureau 6115, Montréal

(Québec) H3K 1G6

![]()

Download our

mobile app

![]()

![]()

Commentaires

Il n'y a pas de commentaires pour le moment.